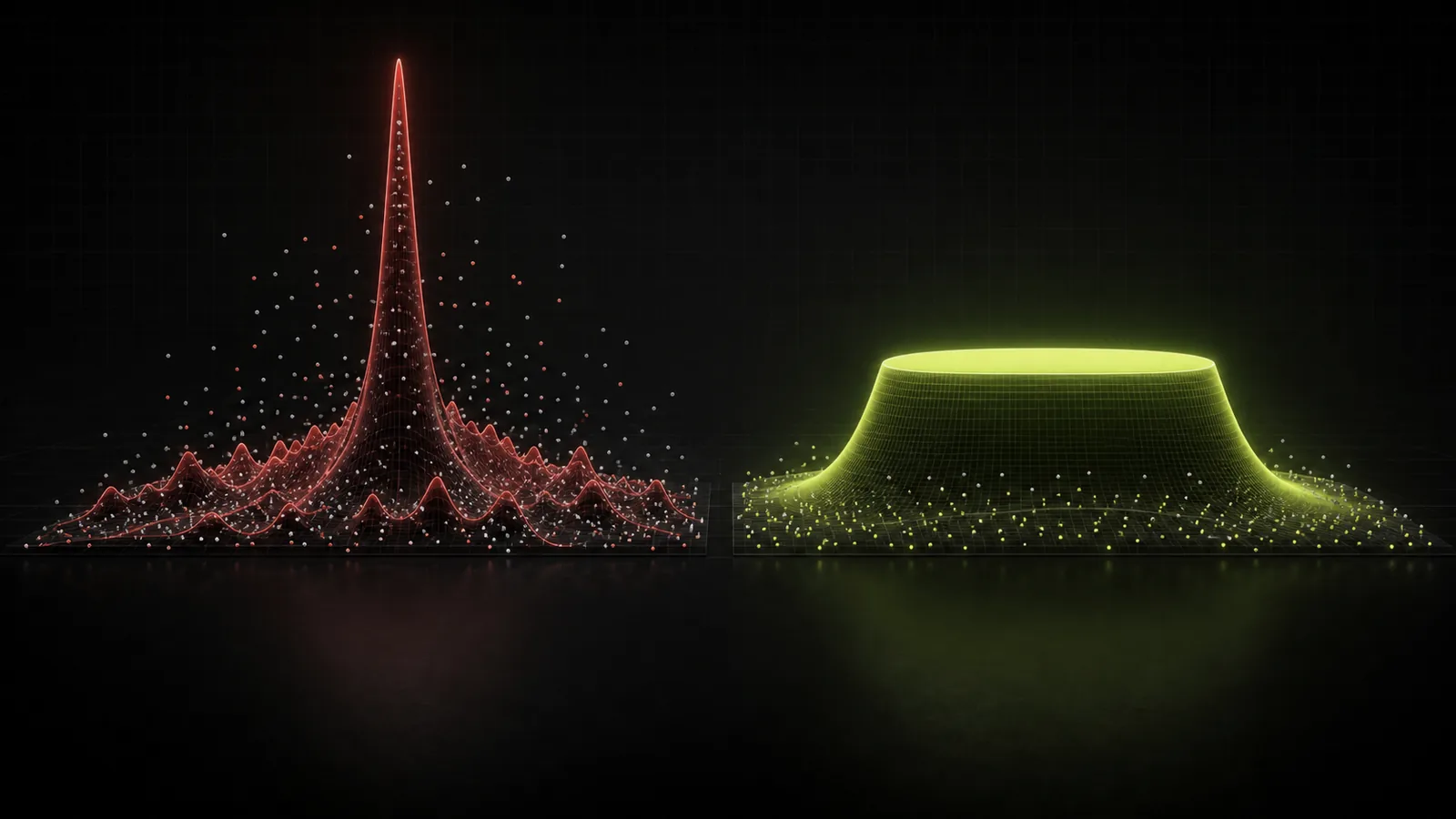

Example 1: Peak versus plateau

Optimising a lookback from 5 to 50, system A peaks sharply at length 13 (expectancy +0.6R) and is negative at 11 and 15. System B is positive and similar across 18 to 30 (expectancy +0.25R, flat). A's headline number is better, but it sits on a needle: live, the future will not land exactly on 13. B's broad plateau is the real edge, because it does not depend on the past's exact accidents.