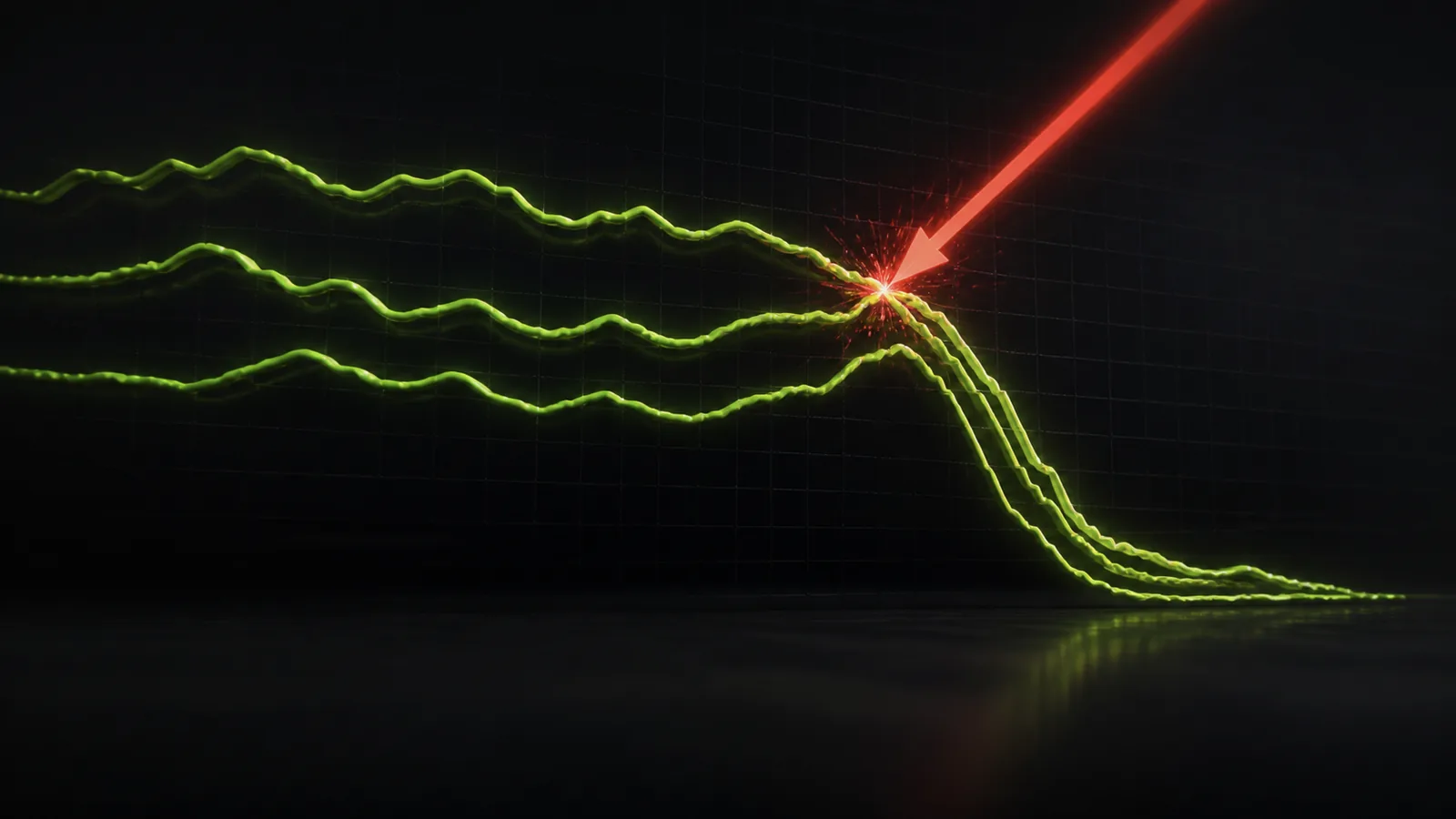

Example 1: Three trades, one real bet

A trader risks one percent each on three different positions that, unknown to them in the moment, are all long the same broad move. It feels like three percent of diversified risk, but because the three rise and fall together, a sharp move against them loses close to three percent at once, the same as a single three percent bet. Had the trader recognised the correlation, they would have treated the trio as one theme with a one percent budget, sizing each at a third, so the combined shock stayed within the risk they intended rather than triple it.